TRIPLING RENEWABLE ENERGY BY 2030 IS POSSIBLE

- Dubai commitments include tripling capacity from renewable sources to 2030

- To hit the target, there are challenges to be addressed and resolved, and current policies must be accelerated

- 2023 was the year of the renewable breakthrough, with 507 GW added and more than 4.1 TW achieved overall

Among the notable achievements of the recent United Nations Conference of the Parties on Climate Change held in Dubai (COP28), certainly can be included the commitment to triple the installed capacity of energy from renewable sources by 2030, provided first in the so-called “Global Pledge,” then in the final decision of the first Global Stocktake.

In light of last year’s global data, according to the International Energy Agency, this goal will be possible. This is what, in a nutshell, the new IEA report, Renewables 2023, highlights.

The world’s capacity to generate electricity from renewable sources is expanding faster than at any time in the past three decades, according to the agency, giving a real chance to reach the goal of tripling global capacity by 2030 that governments set in Dubai.

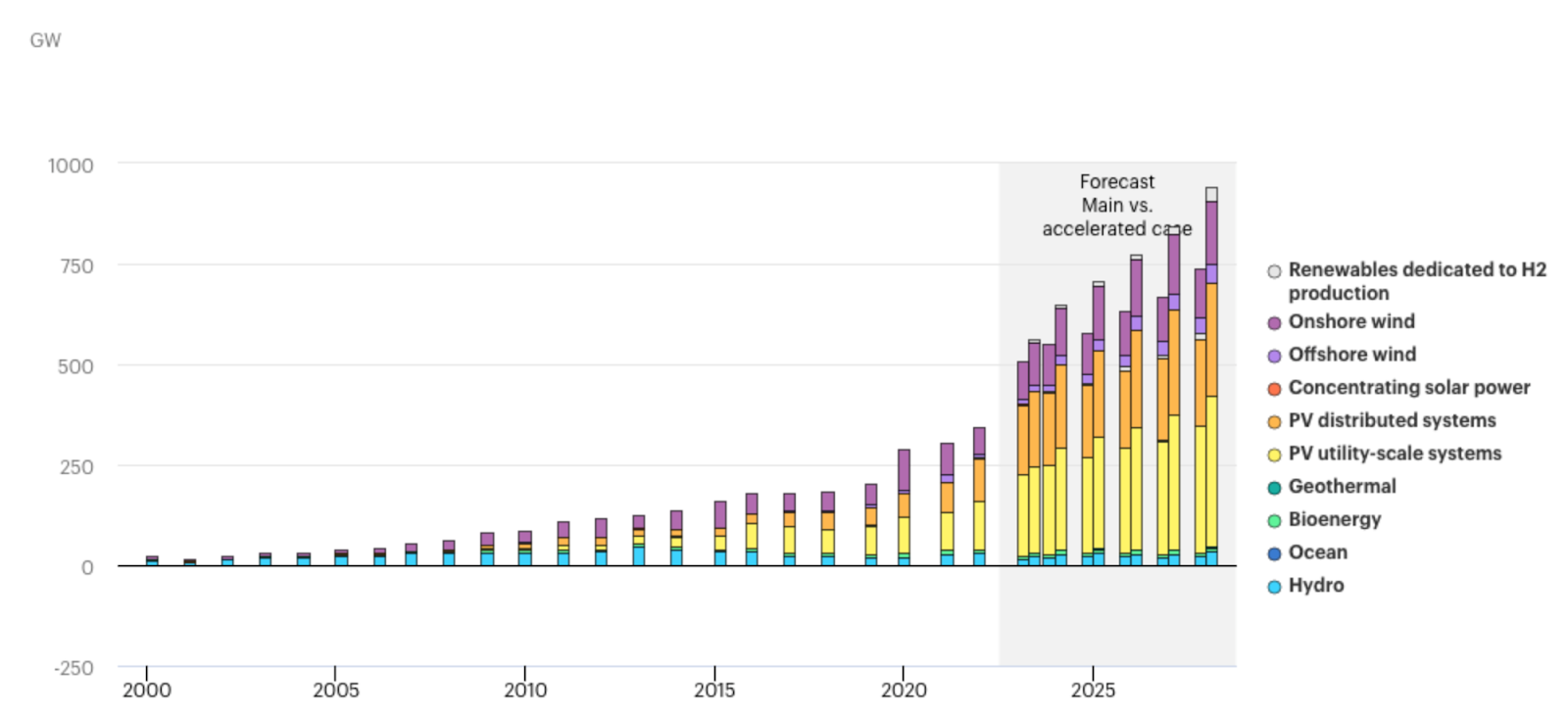

In 2023, total capacity from renewable sources (solar photovoltaic, distributed or scaled; wind, onshore and offshore; hydro, biomass, geothermal, concentrating solar power (CSP), tidal and wave) increased by more than 48%, with 507.43 GW (gigawatts) added worldwide, compared with the previous year. For more than 4.1 TW (terawatts, equivalent to 1 ‘000 GW), total from all sources.

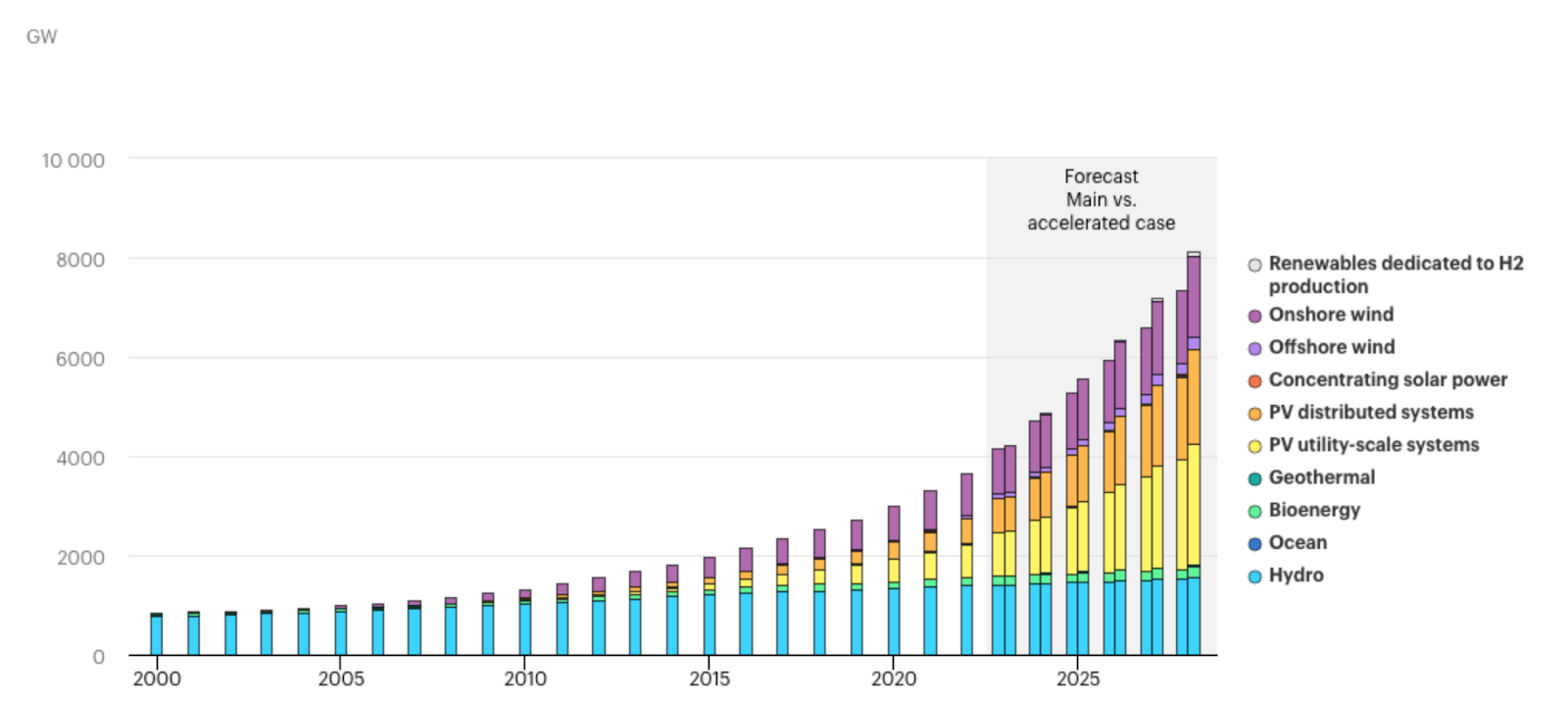

Tripling global renewable capacity in the power sector from 2022 levels by 2030 would lead to more than 11 TW, in line with the IEA’s Net Zero Emissions to 2050 (NZE) scenario.

Current policies, challenges and the need to accelerate

The IEA estimates that under existing policies and market conditions, global renewable capacity is expected to reach 7.3 TW by 2028. This growth trajectory would see global capacity increase to 2.5 times the current level by 2030, missing the target of tripling.

But governments, according to the agency, can close the gap to reach more than 11 ‘000 GW by 2030 by implementing existing policies more quickly and overcoming current challenges that fall into four main categories and vary by country:

1) policy uncertainties and delays in policy responses to the new macroeconomic environment;

2) underinvestment in grid infrastructure that prevents faster expansion of renewables;

3) administrative hurdles, permitting procedures, and social acceptance problems;

4) insufficient financing in emerging and developing economies.

The accelerated case of the Renewables 2023 report, shows that solving these challenges can lead to higher renewables growth of nearly 21%, pushing the world toward achieving the global commitment to triple energy sources.

What is needed to achieve the collective goal of tripling renewable energy by 2030 also varies significantly by country and region, the IEA report says. G20 countries account for nearly 90% of global renewable energy capacity. In the accelerated case, which assumes greater implementation of existing policies and targets, G20 countries could triple their collective installed capacity by 2030. As such, they have the potential to contribute significantly to tripling global renewable energy. However, to reach the global target, the rate of new installations must also accelerate in other countries, including many emerging and developing economies outside the G20, some of which do not have renewable targets and/or supportive renewable energy policies.

2023, the year of the renewable breakthrough

Returning to what happened in 2023, in relation to renewables capacity development, it should be noted that it was an extraordinary year. In fact, data from the International Energy Agency show the following annual increases: 180 GW (2016), 179 (2017), 184 (2018), 204 (2019), 289 (2020), 303 (2021), 342 (2022), and 507 (2023).

As for different technologies, the 507.43 GW increase in new installed capacity in 2023 is composed as follows:

- 375 GW from solar photovoltaics (+64.2%), totaling 1.55 TW;

- 108 GW from wind power (+44.9%), for 1.06 TW total;

- 17 GW from hydro (-45.2%), for 1.41 TW total;

- 6 GW from biomass (-15.5%), for a total of 156.8 GW;

- 483.45 MW from geothermal (+2.65%), totaling 3.26 GW;

- 645 MW from concentrated solar power (CSP) (+3.92%), totaling 2.44 GW;

- the remaining 30 MW total from tidal and wave energy.

As of 2023, therefore, worldwide and among all sources, a total of 4,129.74 GW of generating capacity from renewable sources was installed, including 37.5% solar photovoltaic, 34.2% hydroelectric, and 24.4% wind.

Fig. 1 – Additional capacity

Fig. 2 – Cumulative capacity

Renewable geography

The greatest growth was in China, which put as much solar photovoltaic power into operation in 2023 as the entire world in 2022, while wind power additions -also in China- increased by 66% from the previous year. Increases in renewable energy capacity in Europe, the United States and Brazil also reached all-time highs.

The IEA predicts that the deployment of solar PV and onshore wind between now and 2028 will more than double in the United States, the European Union, India and Brazil, compared with the past five years.

Photovoltaic module prices in 2023 fell by nearly 50% from the previous year, with cost reduction and rapid deployment set to continue. This is because global production capacity is expected to reach 1 ‘100 GW by the end of 2024, significantly exceeding demand.

In contrast, the wind industry (outside of China) is facing a more challenging environment due to a combination of continued supply chain disruptions, higher costs and long permitting times, requiring more policy attention.

Birol: goal will only be achieved if emerging and developing countries are on board

For IEA Executive Director Fatih Birol, “The IEA’s new report shows that under current policies and market conditions, global renewable capacity is already capable of increasing by two and a half times by 2030. That’s still not enough to meet the COP28 goal of tripling renewables, but we are getting closer and governments have the tools they need to close the gap.”

“Onshore wind and solar PV are now cheaper than new fossil fuel plants almost everywhere and cheaper than existing fossil fuel plants in most countries. There are still some major hurdles to overcome, including the difficult global macroeconomic environment. In my view, the most important challenge for the international community is to rapidly increase renewable energy financing and deployment in most emerging and developing economies, many of which have lagged behind in the new energy economy. Success in achieving the tripling goal will depend on it.”

Article by Paolo Della Ventura, Volunteer Italian Climate Network